The leadership of the Tax Committee of Tajikistan refutes claims about the high tax burden in the country, stating that the load remains lower or at the level of most neighboring countries. Is this really the case?

The head of the Tax Committee Nusratullo Davlatzoda stated that the tax burden in the RT remains lower or at the level of most neighboring countries.

“Tajikistan does not have a high tax burden, as is often claimed. We are constantly working on reducing the tax burden to improve business conditions and comply with international standards,” he said at a press conference on February 13.

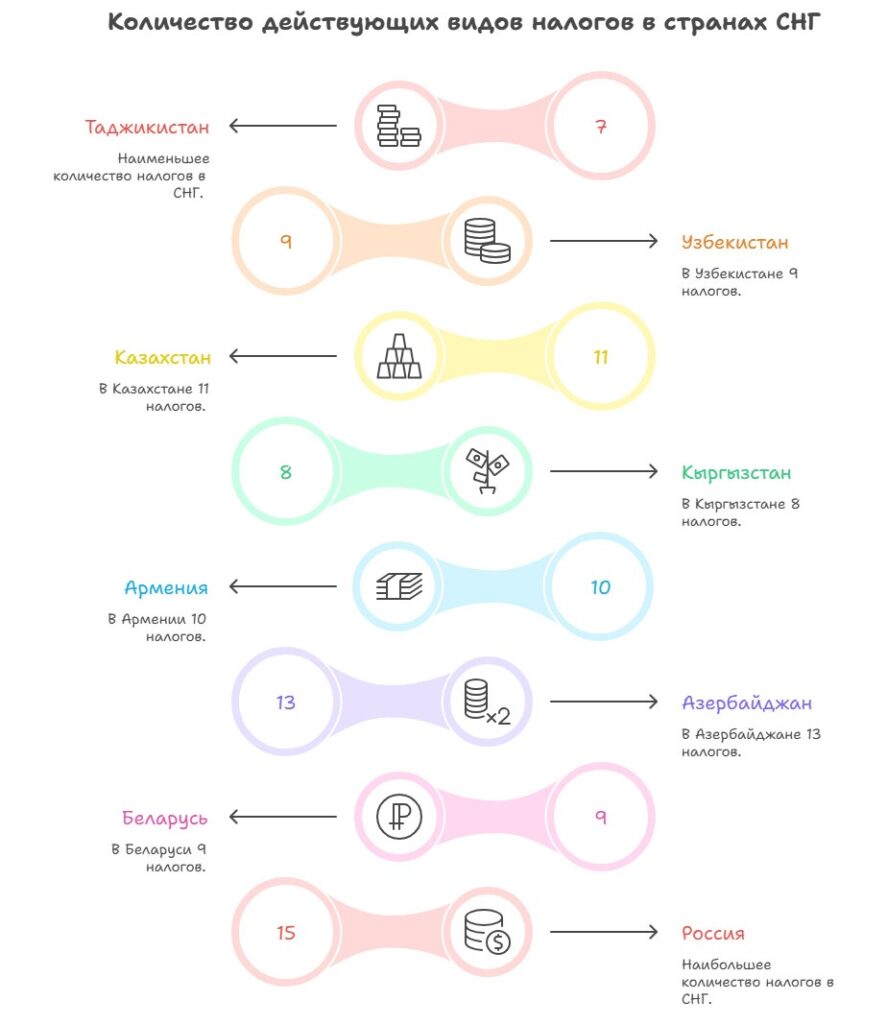

According to him, the state consistently reduces the number of taxes and lowers rates, creating more favorable conditions for entrepreneurs. As an example, he reminded about the 2022 reform: the number of tax types was reduced from 10 to 7, which, according to the head of the committee, significantly simplified the tax system for business.

Davlatzoda also emphasized that the tax burden in Tajikistan is not higher than in neighboring countries.

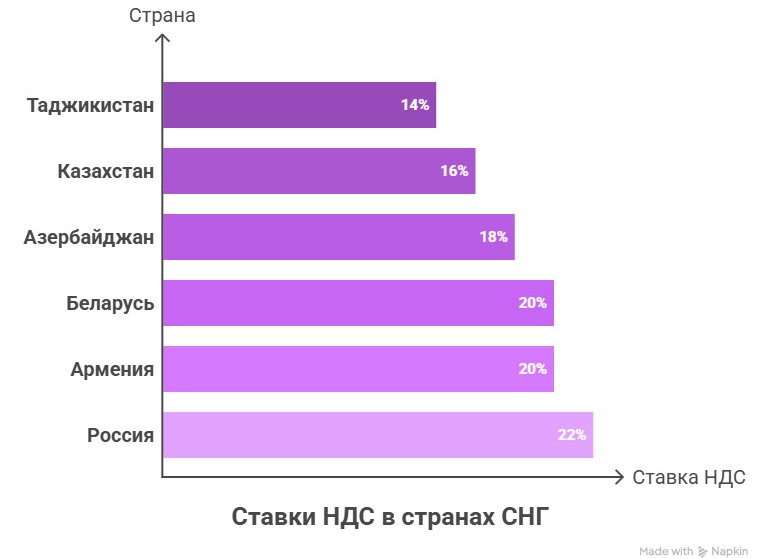

He specifically addressed key tax rates. The VAT rate in Tajikistan in previous years was reduced from 18% to 15%, as of January 1, 2026, it is 14%, and from 2027 it will be reduced to 13%.

The income tax for legal entities in Tajikistan, according to him, has also been optimized:

– for enterprises in the manufacturing sector, the rate has been reduced to 13%;

– for other types of activities — to 18%;

– for mobile companies and financial organizations — to 20%.

In Belarus, Azerbaijan, and Russia, the profit tax rate is 20%, in Armenia — 18%, and in Uzbekistan — 15%.

He also compared income tax rates.

“You see, taxes in Tajikistan do not differ in high burden compared to other CIS countries and main trading partners,” emphasized Davlatzoda.

He added that changes in tax legislation are aimed at further reducing the burden and simplifying administration. According to him, this contributes to improving business conditions, increasing transparency, and helps the country improve its positions in international rankings and attract foreign investments.

“Reducing taxes and simplifying reporting, as well as increasing business transparency, will help strengthen the country’s economy and create new jobs,” noted the head of the Tax Committee.

Fact Checking

Tax systems of different countries vary, there are no two absolutely identical ones, which complicates the direct comparison of the tax burden. Tax rates and rules differ greatly across countries, sometimes even in different regions of the same country.

To determine the real tax burden, various indicators are usually used, mainly tax rates, sometimes the ratio of taxes to GDP.

It should be noted that the number of taxes does not matter much because the tax burden is assessed not by quantity, but by their cumulative impact on payers.

We decided to verify the reliability of the above data based on the rates of the three main taxes (VAT, profit tax, and income tax, which usually form over 60% of tax revenues) of Central Asian countries, as well as the ratio of taxes to GDP.

Kazakhstan

The Tax Code provides for 11 types of taxes.

Profit tax (Corporate income tax):

– the standard rate for most companies — 20%;

– for agricultural organizations under the general regime (sometimes reduced rates for certain regimes/sectors) — 10%.

VAT:

– standard rate — 12%.

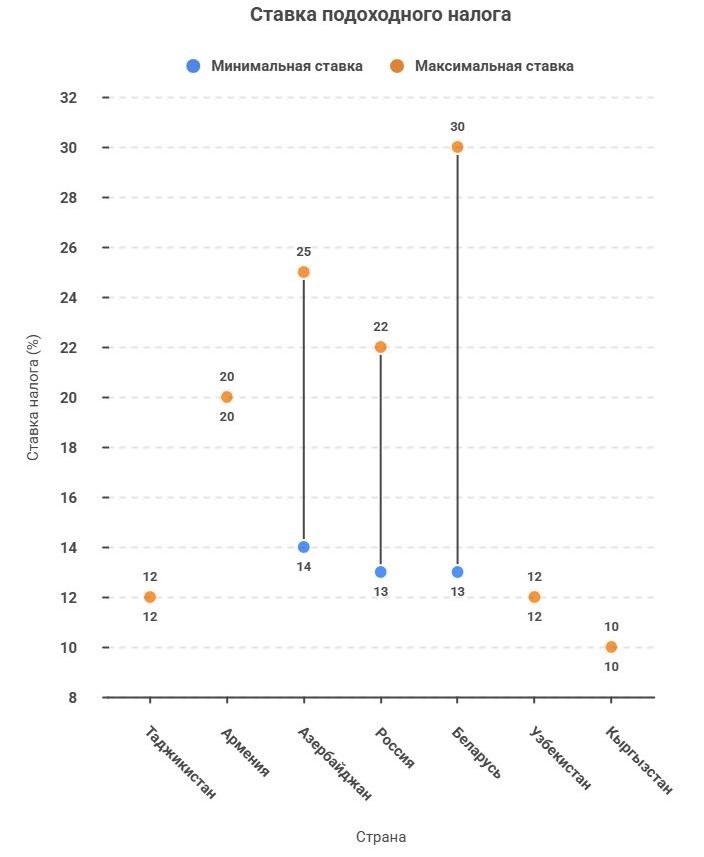

Personal income tax:

– basic rate — 10%.

Kyrgyzstan

There are 7 types of taxes in the country.

Profit tax:

– standard rate — 10%;

– a zero rate may apply to certain types of activities/enterprises with preferences (e.g., ore extraction, investment projects).

VAT:

– standard rate — 12%.

Personal income tax:

– flat rate — 10%.

Tajikistan

The tax legislation establishes 7 types of taxes.

Income tax for legal entities:

– for activities related to the production of goods — 13%;

– for credit and financial organizations and mobile companies — 20%;

– for other types of activities — 18%.

VAT:

– standard rate — 14%.

Personal income tax:

– standard rate — 12%.

Turkmenistan

There are 11 types of taxes.

Profit tax:

– for resident legal entities of Turkmenistan, the rate is 8% (2% for small and medium-sized enterprises);

– for other legal entities — 20% on profits.

VAT:

– standard rate — 15%;

Personal income tax:

– standard rate — 12%.

Uzbekistan

The Tax Code provides for 9 types of taxes.

Profit tax:

– standard rate — 15% (certain rates/exceptions may apply for some categories or under special regimes).

VAT:

– standard rate — 12%.

Personal income tax:

– basic rate — 12%.

Thus, the lowest cumulative tax burden on the three key rates is in Kyrgyzstan. Tajikistan is above the regional average.

The Share of Taxes in GDP

The ratio of taxes to GDP to some extent shows the tax burden. The higher this indicator, the higher the tax burden is considered to be, and vice versa.

Tax revenues to GDP of CA countries in 2025:

Kazakhstan

Tax revenues — $55 billion;

Nominal GDP — $300 billion;

Tax-to-GDP ratio — about 18.3%.

Kyrgyzstan

Tax revenues — $3.5 billion;

Nominal GDP — $22.6 billion;

Tax-to-GDP ratio — 15.5%.

Tajikistan

Tax revenues – about $4 billion;

Nominal GDP — $19 billion;

Tax-to-GDP ratio — 21%.

Turkmenistan

Tax revenues (not available in the public domain);

Nominal GDP — $72.1 billion;

Tax-to-GDP ratio — unknown.

Uzbekistan

Tax revenues — $20.5 billion;

Nominal GDP — $152.5 billion;

Tax-to-GDP ratio — 13.4%.

As the data show, the highest load is in Tajikistan, the lowest is in Uzbekistan. Kazakhstan and Kyrgyzstan occupy an intermediate position, and additional data is needed for Turkmenistan.